Top 5 Austin Real Estate Questions

1. Is Austin officially in a buyer’s market right now?

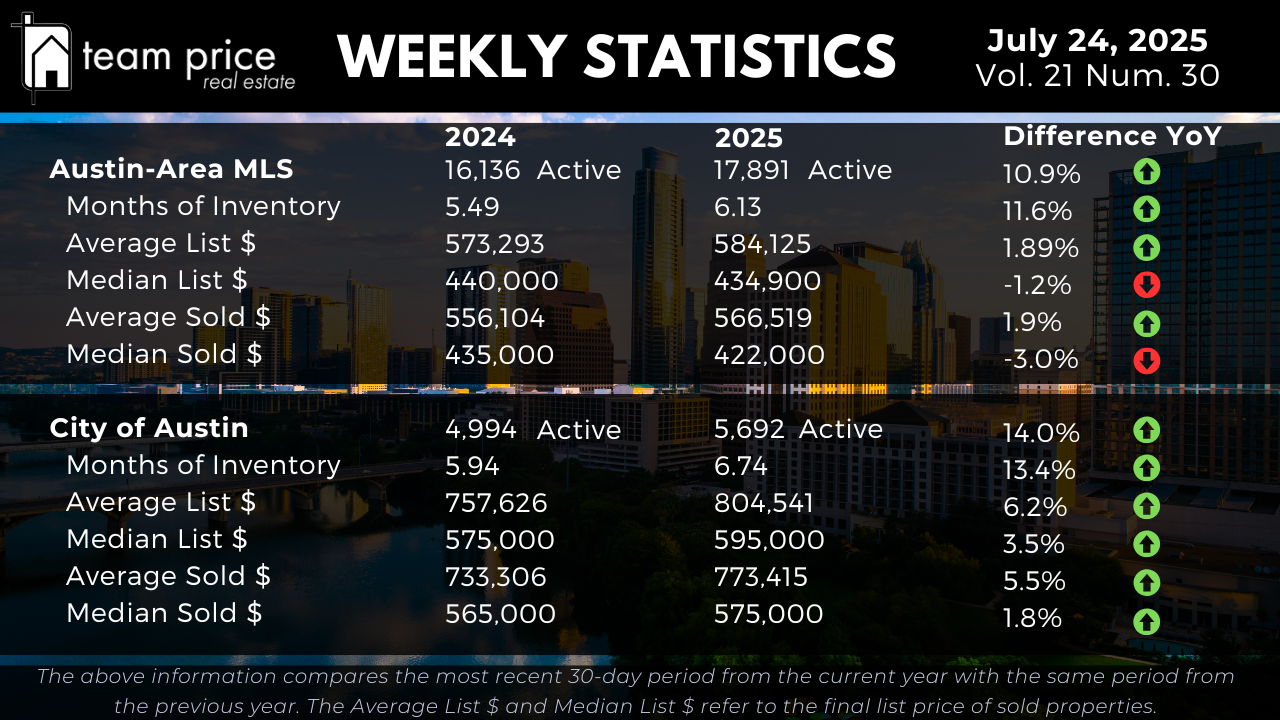

Not yet, but we’re heading that way. Technically, a buyer’s market is defined as having more than seven months of inventory—and right now, the Austin-Area MLS sits at 6.13 months. That’s up from 5.49 just a year ago. In the City of Austin, we’re even closer at 6.74 months. So, while we’re not officially in a buyer’s market, the trajectory is clear. Buyers are gaining leverage. Homes are staying on the market longer, sellers are negotiating more, and price sensitivity is creeping back into nearly every price point. If this trend continues, we’ll likely cross that seven-month threshold soon, which would mark a formal transition into buyer-market conditions.

2. How much negotiating power do buyers have right now?

Buyers have more leverage today than they’ve had in years. Nearly 70% of homes across the Austin-Area MLS are now selling below their asking price. That’s a notable shift from where we were a year ago, and even a few months ago. The average sold-to-list price ratio is currently at 97.19%, which means sellers are typically accepting offers about three percent below what they listed for. On top of that, only about 18% of homes are closing at full list price, and less than 13% are going over asking. For buyers, this translates into more room to negotiate, more time to make decisions, and less pressure to rush into offers—especially in price points above $500,000 where competition has thinned out.

3. Are higher-end homes holding value better than mid-range homes?

They are, and that’s an important nuance in the market right now. When you look at the average sold price in the Austin-Area MLS, it's up 1.9% year over year, sitting at around $566,519. But the median sold price—which represents the true middle of the market—is actually down three percent, now at $422,000. What that tells us is that the higher-end homes are skewing the averages upward, while the broader middle of the market is still under pressure. We’re seeing the same trend in the City of Austin. Average prices have jumped 5.5% to just over $773,000, but the median is only up 1.8%, landing at $575,000. That spread reveals what’s really happening: the luxury tier is still moving, often with cash or jumbo loan buyers, while the mid-market is where affordability is tightest and price resistance is strongest.

4. Are most neighborhoods in Austin stabilizing, or are we still in a correction?

We’re still in a correction across most of the metro. It’s uneven, and while some pockets are starting to stabilize, the broader trend is still one of price softness. Across 30 tracked cities in the area, only 11 posted a month-over-month price gain, while 19 saw declines. That means about two-thirds of the cities are still moving backward in terms of value. When we zoom in to the ZIP code level, about 53% showed price increases over the past month—but 47% declined. Only two ZIP codes have surpassed their price peaks from the past 12 months. That’s critical. It shows that while you might find a few bright spots—usually in low-inventory neighborhoods or high-demand school zones—the majority of the market hasn’t recovered peak pricing. The correction isn’t over, even if it’s not as sharp as it was in late 2022.

5. How far are prices from their peak, and are we likely to return there soon?

Prices are still well below their peak, and there’s no evidence yet that we’re heading back to those highs anytime soon. In the Austin-Area MLS, the median sold price has fallen about 19% from the peak of $538,000 in May 2022 to $435,000 today. The average sold price is down roughly 12.6% from its high. When you break it down by price per square foot, the drop is even steeper—over 18% lower for the average and more than 23% down for the median. In the City of Austin, we’re seeing a similar pattern. The median sold price peaked at $680,000 and now sits at $575,000, which is about a 15% decline. Price per square foot in Austin is down more than 20%. So, even though some sellers are holding the line on list prices, the actual sold data confirms we’re still in a lower-value cycle. This isn’t a crash, but it is a real and measurable market reset.